The DRC Is About to Become One of the World's Largest Lithium Producers. The Manono Project Is Not a Development Story. It Is a Control Story.

Ready

Zijin Mining's USD 1.4 billion lithium project in the Manono region of the Democratic Republic of Congo will produce approximately 130,000 tonnes of lithium carbonate equivalent annually, potentially accounting for close to 5 percent of global supply by 2028. It includes a processing facility converting concentrate into lithium sulphate. It is contested by a dispossessed Australian miner and coveted by Bezos-backed KoBold Metals. Understanding what Manono actually represents requires looking past the production numbers to the ownership architecture, the processing question, and what the legal battles signal about how seriously the world is competing for this deposit.

Why Manono Matters Beyond the Numbers

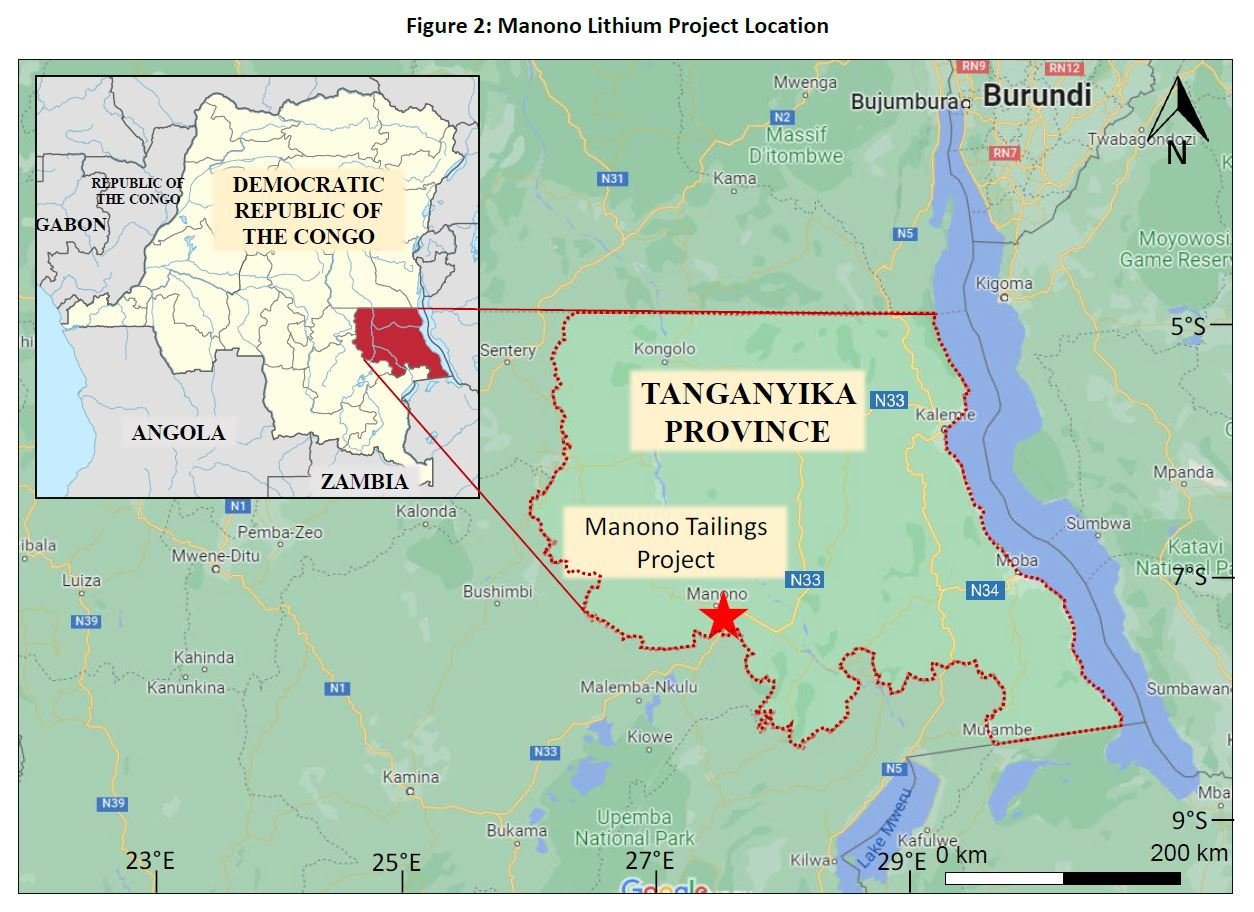

The Manono lithium deposit in Tanganyika Province sits within one of the most geologically extraordinary mineral concentrations on earth. The DRC already produces over 70 percent of the world's cobalt. It holds copper reserves of continental significance. And in the Manono region, it holds a lithium pegmatite deposit whose scale, measured in contained lithium carbonate equivalent, places it among the largest hard rock lithium resources identified anywhere globally.

The Zijin Mining Group project now advancing toward production at Manono is expected to produce approximately 130,000 tonnes of lithium carbonate equivalent annually at full capacity, a volume that would represent close to 5 percent of projected global lithium supply by 2028. At a capital investment of USD 1.4 billion, it is one of the largest single mining investments currently active in Central Africa. It includes a processing facility designed to convert 500,000 tonnes of lithium concentrate annually into lithium sulphate, an intermediate battery chemistry input.

These numbers are significant in aggregate. But the most analytically important things about Manono are not in the production projections. They are in the ownership structure, the processing question, the legal disputes surrounding the licence, and what the combination of these factors reveals about who actually controls one of the DRC's most valuable emerging resource assets and on what terms.

The Manono project is not primarily a story about lithium production. It is a story about how Africa's most consequential mineral deposits are being structured, contested, and controlled at a moment when the geopolitical and commercial stakes of that control are higher than at any point in the continent's resource history.

Lithium's Transformation From Commodity to System Input

To understand why Manono has attracted the level of investor attention, legal contestation, and geopolitical interest that it has, it is necessary to understand what lithium has become in the global industrial economy over the past decade.

Lithium was, until relatively recently, a specialist commodity used primarily in ceramics, glass, and industrial lubricants, traded in relatively thin markets by a small number of producers supplying a concentrated base of industrial buyers. The commercialisation of lithium-ion battery technology at automotive scale transformed that market structure fundamentally. Every electric vehicle battery contains between 8 and 15 kilograms of lithium carbonate equivalent, depending on battery chemistry and size. Every grid-scale energy storage installation requires lithium at volumes that dwarf the historical consumption of the non-battery industrial market. Every consumer electronics device, from smartphones to laptops, contains lithium-ion cells whose combined global demand now constitutes the largest single application of the mineral.

The International Energy Agency projects that lithium demand will increase between six and ten times by 2040 relative to 2020 levels, depending on the pace of electric vehicle adoption and grid storage deployment. The supply required to meet that demand does not exist in committed production. It requires the development of deposits that are currently in exploration or early development stages, and the Manono deposit, with its scale and grade, is among the most strategically significant of those uncommitted resources globally.

This transformation of lithium from commodity to system-critical input has direct implications for how Manono should be understood. A deposit that produces a commodity is an economic asset whose value fluctuates with market prices. A deposit that produces a system-critical input is a geopolitical asset whose control confers leverage over the industrial systems that depend on it. The DRC, which already holds this kind of leverage in cobalt through the Katanga Copperbelt, is now acquiring a second and potentially larger form of it through its lithium endowment. The question of who controls that leverage, and on what terms it is exercised, is not merely a commercial question. It is a strategic one that extends well beyond the DRC's borders.

Zijin, Ownership, and the Distance Between Equity and Control

Zijin Mining Group, one of China's largest diversified mining companies, holds just under 55 percent of the Manono project through its investment vehicle, with the Congolese state retaining a significant equity position through its state mining vehicles. On the surface, this ownership structure reflects the kind of national participation that resource nationalism advocates have long demanded: the state holds equity in major resource developments rather than simply collecting royalties and taxes on production controlled entirely by foreign investors.

The analytical limitation of equity ownership as a measure of genuine control is precisely what the Manono ownership structure illustrates. Control of a mining project is not determined by share register alone. It is shaped by who provides the development capital and therefore holds debt claims over the project's assets. It is shaped by who holds the technical expertise for mine design, processing plant operation, and quality management. It is shaped by who controls the downstream processing and refining infrastructure that converts the project's output into battery-grade material. And it is shaped by who holds the long-term offtake agreements that determine where the project's production goes and at what price.

On each of these dimensions, the Congolese state's equity position in Manono does not translate directly into operational control. Zijin brings the development capital, the engineering expertise, and the integration with Chinese processing and battery supply chains that give the project's output a defined route to market. The state holds equity claims on the project's cash flows, subject to the cost recovery and profit sharing arrangements embedded in the development agreement. It does not, in the normal course of this ownership structure, hold the technical capability to operate the facility independently, the processing infrastructure to refine the lithium sulphate into battery-grade material, or the market relationships to sell the output outside the supply chain architecture that Zijin provides.

This is not a criticism of the structure as negotiated. It reflects the genuine constraints that resource-holding governments face when they lack the technical expertise, the processing infrastructure, and the market relationships that advanced mining investors bring. But it is precisely the OPEC parallel that Uchumi360's broader critical minerals analysis has identified: ownership exists, control is more complex, and the distance between the two is where value capture is determined.

The processing facility that Zijin is building at Manono, converting concentrate into lithium sulphate, represents a genuine and meaningful step beyond raw concentrate export. Lithium sulphate is an intermediate battery chemistry product that sits higher in the value chain than spodumene concentrate, and its production within the DRC means that some processing value is retained domestically rather than transferred to offshore refineries. But lithium sulphate is not battery-grade lithium hydroxide or lithium carbonate, the forms required directly by battery cathode manufacturers. The conversion from lithium sulphate to battery-grade material, involving further chemical processing and purification steps, will occur in processing facilities that are overwhelmingly located in China. The DRC captures the mining margin and the intermediate processing margin. The highest-value conversion steps happen elsewhere.

The AVZ Dispute and KoBold Interest: What the Contestation Reveals

The most revealing dimension of the Manono story is not in Zijin's production projections or the processing facility specifications. It is in the legal battles and competing interests that surround the deposit, because the intensity of that contestation is a direct measure of how seriously the world's most sophisticated mineral investors assess the deposit's strategic value.

AVZ Minerals, an Australian junior mining company, had previously held exploration and development licences over the Manono deposit and had conducted substantial exploration work establishing the resource's scale and grade. The revocation of AVZ's licence prior to Zijin's entry into the project has resulted in international arbitration proceedings in which AVZ is seeking compensation for the loss of its development rights. The legal process is ongoing and its outcome will have implications not only for the Manono project but for the broader question of licence security and investor protection in the DRC's mining sector.

The AVZ situation illustrates a tension that is not unique to the DRC but that the DRC's governance environment makes more acute than in more institutionally stable mining jurisdictions. The geological and commercial value of a deposit like Manono creates incentives for licence reallocation that can outweigh the reputational and legal costs of revocation, particularly when the incoming investor brings the state capital, political relationships, and supply chain integration that the outgoing licence holder cannot match. Whether the revocation of AVZ's licence reflected legitimate regulatory grounds or represented a more contested process is a matter of ongoing legal dispute. What is not in dispute is that the outcome redirected control of one of the world's most significant lithium deposits from a Western junior miner to a Chinese state-backed major.

Separately, KoBold Metals, the AI-driven exploration company backed by Jeff Bezos, Bill Gates, and a network of strategically motivated investors, has expressed interest in adjacent sections of the Manono deposit. KoBold's presence in the Manono geography is consistent with its broader African critical minerals strategy, which Uchumi360 documented in its analysis of the Mingomba copper project in Zambia. KoBold's interest in Manono represents the Western capital's attempt to establish a presence in the DRC's lithium geology at a time when Zijin's control of the primary deposit has already been consolidated. The commercial and geopolitical significance of having both Chinese state-backed capital and US-aligned strategic capital competing for different sections of the same lithium deposit is a precise illustration of the broader supply chain competition that is playing out across Africa's critical minerals geography.

The combination of the AVZ legal dispute and KoBold's adjacent interest signals something important about Manono that production statistics alone cannot convey: this deposit is contested at the highest level of the global critical minerals competition, by actors whose motivations extend well beyond commercial mining returns into the strategic supply chain positioning that will shape the global battery economy for decades.

The Regional System That Manono's Output Will Move Through

The Manono deposit is located in Tanganyika Province in southeastern DRC, approximately 400 kilometres north of the Zambian border and roughly 1,500 kilometres from the Tanzanian coast. Its output does not reach global markets through DRC infrastructure alone. It moves through a regional logistics system that spans multiple sovereign jurisdictions and whose efficiency, reliability, and cost structure significantly affect the project's commercial performance and the value that the DRC ultimately captures from its lithium endowment.

The primary export routes from Manono run southward through Zambia toward Dar es Salaam via the Tanzania-Zambia Railway and the Central Corridor road network, or southward toward Durban and Beira through the southern African logistics corridors. Each route involves transit infrastructure in countries other than the DRC, whose condition, tariff structures, and operational reliability affect the delivered cost of Manono's output and therefore the commercial margins available to the project and the state.

This logistics dependency means that Tanzania's Central Corridor infrastructure investment, Zambia's railway rehabilitation programmes, and the port capacity at Dar es Salaam are not peripheral to the Manono story. They are integral to it. A processing facility that produces lithium sulphate in Tanganyika Province needs reliable, affordable transport to the coast to compete commercially with lithium production in Australia, where port infrastructure is adjacent to mining operations, and in Chile and Argentina, where coastal or near-coastal deposits reduce logistics costs substantially.

The broader regional opportunity that Manono's scale creates is the potential to anchor regional processing and logistics investment that would benefit multiple mineral flows simultaneously. A rail and road corridor capable of moving Manono's lithium sulphate to Dar es Salaam at competitive cost is the same infrastructure that moves Zambian copper cathode, Tanzanian graphite, and Rwandan tantalum. The investment case for upgrading that corridor is stronger when the additional traffic from a project of Manono's scale is factored in, and Tanzania and Zambia's ability to capture transit and logistics value from the DRC's lithium production depends on their infrastructure being competitive with southern African alternatives.

The Processing Question: What Lithium Sulphate Does and Does Not Represent

The inclusion of a processing facility at Manono converting concentrate into lithium sulphate deserves more precise analysis than either uncritical celebration or dismissive caution. It is a genuinely meaningful step in the right direction, and understanding exactly what it means and what it does not requires clarity about where lithium sulphate sits in the battery value chain.

Natural spodumene concentrate, the first-stage product from hard rock lithium mining, is a physical mineral product containing approximately 6 percent lithium oxide by weight. It is the form in which most hard rock lithium has historically been exported from producing mines, primarily in Australia, for conversion to battery-grade chemical forms in processing facilities primarily in China. Converting concentrate to lithium sulphate at the mine site rather than exporting concentrate for offshore conversion represents a genuine step up the value chain, adding chemical processing value within the DRC rather than transferring it to the importing country.

Lithium sulphate, however, is an intermediate chemical product rather than a battery-ready material. Battery cathode manufacturers require lithium hydroxide monohydrate or lithium carbonate at battery grade, forms that require further chemical processing from lithium sulphate through precipitation, purification, and crystallisation steps. The processing facilities that perform these conversions at commercial scale are overwhelmingly located in China, which controls the majority of global lithium chemical conversion capacity. Manono's lithium sulphate will, absent the development of alternative conversion infrastructure, feed into this Chinese processing system before it reaches battery manufacturers.

The distinction matters for value capture. The DRC captures the mining margin and the concentrate-to-sulphate conversion margin through the Manono processing facility. The sulphate-to-hydroxide or sulphate-to-carbonate conversion margin, and all downstream value above that, is captured by the processing and manufacturing facilities that sit between Manono's output and the electric vehicle or grid storage system that ultimately uses the lithium. The processing facility at Manono is a meaningful improvement over pure concentrate export, but it is not the processing integration that captures the battery economy's full value premium for the DRC.

The more ambitious processing trajectory for Manono, and for DRC lithium production more broadly, would involve the development of lithium chemical conversion facilities producing battery-grade hydroxide or carbonate within the DRC or within the immediate regional geography. This requires energy at industrial scale, technical expertise in lithium chemical processing, and market relationships with battery manufacturers that accept African-produced battery-grade lithium as a qualified supply source. Each of these requirements is achievable but not automatic, and achieving them requires deliberate policy and investment strategy over a longer horizon than the current project development timeline.

What Manono Signals About Africa's Critical Minerals Trajectory

The Manono project, read in full context, is simultaneously more significant and more complicated than either optimistic or pessimistic framings suggest. It is more significant because a deposit of this scale, producing at 5 percent of global lithium supply, genuinely changes the DRC's position in the global lithium market and creates the kind of production anchor around which regional processing and logistics investment can be organised. It is more complicated because the ownership structure, the processing limitations, the legal contestation, and the logistics challenges collectively mean that the value capture question remains genuinely open rather than settled in the DRC's favour by the project's existence.

The pattern visible in Manono is consistent with the pattern Uchumi360's critical minerals analysis has identified across the region: Africa's mineral endowment is increasingly central to the global energy transition, the capital to develop that endowment is available, and the structural question of who captures the value that production generates is the variable that will determine whether this resource cycle produces a different outcome from the petroleum era.

Manono is the DRC's most visible test case of this question in lithium. The processing facility represents partial progress on the value addition agenda. The ownership structure reflects the genuine constraints on state control in the absence of technical and financial capacity that would support independent development. The legal disputes reflect the intensity of the global competition for the deposit's control. And the logistics challenge reflects the regional infrastructure gaps that affect every major mineral project in the inland African geography.

The trajectory of Manono's development, specifically whether the processing facility is followed by further chemical conversion investment, whether the ownership structure evolves toward greater DRC technical capability as the project matures, and whether the legal framework protecting licence holders is strengthened by the AVZ proceedings' outcome, will be a meaningful indicator of whether the DRC is building a lithium economy or simply a lithium extraction industry.

The scale is real. The strategic significance is real. The value capture question is where the story is still being written.

______________________________________________________________________________________

Sources: Zijin Mining Group Manono Project Disclosures and Annual Reports, DRC Ministry of Mines Licence and Production Data, AVZ Minerals International Arbitration Filings and ASX Disclosures, KoBold Metals Project Portfolio Statements, International Energy Agency Global Lithium Supply and Demand Outlook 2024, Benchmark Mineral Intelligence Lithium Price and Supply Chain Analysis, African Development Bank DRC Mining Sector Assessment 2024, World Bank Critical Minerals for Climate Action Report 2023, Tanzania Central Corridor Logistics Authority Data, TAZARA Railway Capacity and Operations Reports.

_______________________________________________________________________________________

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely. Add payment credentials to enable checkout here.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.