Kenya Built LAPSSET to Win East Africa's Logistics Future. Tanzania May Have Already Won It.

Ready

The Lamu Port-South Sudan-Ethiopia Transport Corridor was conceived as Kenya's boldest infrastructure bet, a second strategic gateway that would reposition the country as the dominant trade and logistics hub for East and Central Africa. Nearly a decade after construction began, the corridor remains incomplete, its northern logic is under geopolitical stress, and Tanzania has used the intervening years to build a competing infrastructure architecture that is quietly capturing the regional trade flows LAPSSET was designed to serve.

The Premise and the Promise

When Kenya's government formally launched the LAPSSET Corridor Programme, the strategic logic was compelling and the timing appeared right. The Northern Corridor, running from Mombasa through Nairobi to Malaba and westward to Kampala, Kigali, and Bujumbura, had served as East Africa's primary trade artery for decades. But it was concentrated in a narrow geographic band covering approximately 150 kilometres of Kenya's total land mass, leaving the northern and north-eastern regions of the country, which account for over 70 percent of its territory, economically disconnected from the national and regional economy.

LAPSSET was designed to correct this in a single infrastructure programme of extraordinary ambition. A 32-berth port at Lamu on the Indian Ocean coast. Standard gauge railway lines running from Lamu northward to Isiolo, then branching to Moyale on the Ethiopian border and to Nakodok on the South Sudan border. A crude oil pipeline from Kenya's Lokichar basin northward to Lamu for export. A product oil pipeline serving Ethiopia's market. Highways following the same corridors. International airports at Lamu, Isiolo, and Turkana. Resort cities at each node to generate the economic activity that would make the infrastructure commercially viable. Special economic zones and industrial parks along the corridor's length to create the cargo that would justify the railway and road investment.

The programme's regional logic was equally ambitious. By creating a second strategic corridor serving Ethiopia and South Sudan, Kenya would extend its logistics dominance beyond the countries already served by the Northern Corridor, capture the trade of over 100 million people in the Horn of Africa hinterland, and position Lamu as a regional hub competing with Djibouti for the traffic of landlocked Ethiopia, the world's second most populous landlocked country. By connecting to South Sudan's oil fields through the crude pipeline, Kenya would monetise the Lokichar basin discoveries and anchor the port's commercial viability through guaranteed energy export volumes.

It was, on paper, one of the most strategically coherent infrastructure programmes in East African history. The gap between that paper logic and the execution reality of the intervening years is where the story becomes analytically important.

What Has Been Built, What Has Not, and Why the Gap Matters

The honest assessment of LAPSSET's progress requires distinguishing between the components that have advanced materially and those that remain at planning or early construction stage, because the corridor's strategic value depends on the system working as an integrated whole rather than on individual components in isolation.

The Lamu Port's first three berths represent the programme's most concrete achievement. Construction on the initial berths began in earnest in 2016 and the first berth came into operation, with subsequent berths following. The port now handles general cargo and has the physical infrastructure of a functioning deep-water facility. The port headquarters and auxiliary facilities are in place, power connection from the national grid has been established, and the basic operational framework is functioning.

The highway network has seen more progress than is commonly acknowledged. The Isiolo to Moyale road, approximately 505 kilometres connecting Kenya's central highlands to the Ethiopian border, was completed by 2016 and represents a genuinely completed component of the corridor that has improved connectivity for northern Kenya and simplified cross-border road transport with Ethiopia. Sections of the northern highway network have been contracted and partially constructed. The physical road infrastructure serving the Ethiopian direction is more advanced than the railway or pipeline components.

The railway component, which represents the highest-value and highest-cost element of the corridor's transport infrastructure, remains the most incomplete. The standard gauge railway lines connecting Lamu to Isiolo and extending to the Ethiopian and South Sudan borders were at preliminary design stage as of 2017, and while there has been subsequent planning and coordination activity, the railway has not been built at the scale the programme envisioned. Without the railway, LAPSSET functions as a road corridor with a port, not the multimodal transport system whose economics were used to justify the investment.

The crude oil pipeline, which was the financial anchor for the entire programme in its original conception, has encountered the most significant delays. The Lokichar to Lamu pipeline was initially planned for completion around 2021 to 2022. It has not been completed. The reasons are multiple and interconnected: the complexity of the joint development agreement between the government and the oil companies including Tullow Oil, the financing challenges of a large cross-country pipeline in a frontier market, and the shifting economics of Kenyan upstream development as global oil price cycles and carbon transition pressures have changed the investment calculus for East African oil development.

The absence of the pipeline matters enormously for LAPSSET's commercial logic because it was the guaranteed cargo volume that was supposed to anchor Lamu Port's revenue base and justify the railway investment. A 32-berth port serving general cargo in a region where the competing Mombasa port is far better established, far better connected to existing road and rail infrastructure, and far closer to the primary demand centres of East Africa, faces a genuinely difficult commercial challenge without the captive pipeline traffic that the original plan assumed.

The South Sudan Variable: When Geopolitics Undermines Infrastructure Logic

LAPSSET's northern architecture, the railway and pipeline connections to South Sudan, was premised on a political assumption that has not held. South Sudan, which achieved independence in 2011, was expected to develop into a stable, oil-exporting economy that would generate substantial transit traffic through the LAPSSET corridor. The country's oil fields, whose crude would flow through the Nakodok to Lokichar to Lamu pipeline in the programme's full vision, represented the northern anchor of the corridor's cargo logic.

South Sudan's trajectory has instead been defined by recurring conflict, economic collapse, and the kind of political instability that makes long-horizon infrastructure investment planning extraordinarily difficult. The country has experienced civil war, peace agreements that have held imperfectly, and persistent governance fragility that has kept its oil production well below potential and its economy in a condition that generates far less transit trade than the LAPSSET projections assumed.

The South Sudan variable is not merely a setback for one component of LAPSSET. It undermines the entire northern logic of the corridor. The railway to Nakodok, the pipeline from Jonglei, and the substantial portion of Lamu Port's projected cargo volumes that depended on South Sudanese trade and oil exports cannot materialise on the original timeline as long as South Sudan remains in its current condition. This has shifted the weight of LAPSSET's viability entirely onto the Ethiopian connection, which is more robust economically but represents a different competitive dynamic from the one the programme's original architecture assumed.

Ethiopia is the second most populous country on the African continent and one of its fastest-growing economies. Its landlocked geography creates genuine and large demand for efficient access to ocean ports, and the Kenya-Ethiopia relationship has deepened significantly in trade and investment terms over the past decade. The Moyale corridor, connecting Ethiopia's southern regions to Lamu through the completed Isiolo to Moyale highway, is the component of LAPSSET that has the most immediate commercial relevance. But Ethiopia also has Djibouti, which handles the overwhelming majority of its import and export trade through a port and railway connection that is established, functioning, and deeply embedded in Ethiopian supply chains. Diverting a meaningful proportion of Ethiopian trade through Lamu requires LAPSSET to offer a competitive combination of cost, reliability, and transit time that it has not yet demonstrated at scale.

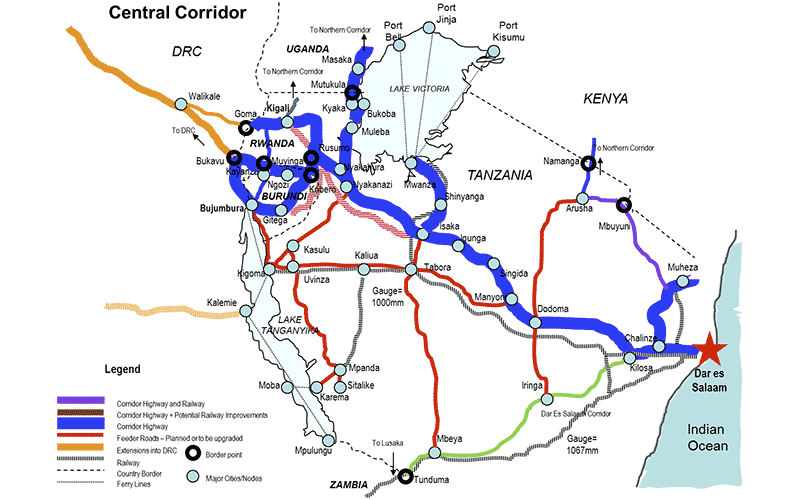

Tanzania's Counter-Move: The Central Corridor's Quiet Advance

While LAPSSET has been navigating its execution challenges, Tanzania has been building the infrastructure that makes its Central Corridor an increasingly compelling alternative for the regional trade flows that both corridors are competing to serve. The strategic implications of this parallel development are significant and insufficiently analysed in the regional infrastructure discourse.

The Central Corridor runs from the port of Dar es Salaam westward through Tanzania to the borders of Uganda, Rwanda, Burundi, and the DRC. It serves a hinterland that overlaps substantially with the markets LAPSSET was designed to reach, specifically the landlocked countries of the Great Lakes region whose trade currently flows through either Mombasa and the Northern Corridor or Dar es Salaam and the Central Corridor. The competition between these two corridor systems for the transit trade of Uganda, Rwanda, Burundi, and eastern DRC is one of the most consequential but least discussed infrastructure competitions in the region.

Tanzania's Julius Nyerere Hydropower Station, when fully operational, improves the energy position of the corridor's industrial zones and reduces the power cost constraints that have historically limited manufacturing investment along the Central Corridor route. The Tanzania Standard Gauge Railway, whose first phase connects Dar es Salaam to Dodoma and is extending westward toward the Isaka dry port and eventually to the Rwandan and Burundian borders, represents a direct investment in the multimodal transport capability that LAPSSET's railway was supposed to provide along the northern route.

Dar es Salaam Port has undergone substantial expansion and operational improvement over the past decade, with berth additions, container terminal upgrades, and port management reforms that have reduced vessel turnaround times and improved the port's competitiveness relative to its historical performance. The Tanzania Ports Authority has been active in developing Dar es Salaam as a logistics hub, and the port's throughput has grown consistently as regional trade volumes have increased.

The competitive implication of Tanzania's infrastructure advance is that the regional trade flows LAPSSET was designed to capture, specifically the transit trade of Rwanda, Burundi, Uganda, and the DRC, have not been waiting for LAPSSET to be completed. They have been flowing through whichever corridor offers the best combination of cost, reliability, and transit time at any given moment, and Tanzania's infrastructure investment has been systematically improving the competitiveness of the Central Corridor option. Every container that moves from Dar es Salaam to Kigali rather than from Mombasa to Kigali is a data point in a commercial competition that LAPSSET's incomplete state makes it structurally difficult to win.

The DRC: The Largest Prize in the Corridor Competition

The Democratic Republic of Congo deserves particular attention in the corridor competition analysis because it represents the largest single potential cargo market in the region and the one whose routing decision has the greatest long-term implications for whichever corridor secures its trade.

The DRC's mining sector, centred on the Copperbelt and Kasai provinces in the south and centre of the country, generates export volumes of copper, cobalt, and other minerals that constitute some of the most significant cargo flows in the region. The routing of those exports, whether through Dar es Salaam via the Central Corridor, through Durban or Beira via southern routes, or eventually through Lamu via a fully completed LAPSSET system, is determined by a combination of infrastructure quality, transit cost, and reliability that shifts as competing corridor investments progress.

Tanzania's geographic position gives it a natural advantage for eastern DRC trade. The distance from Lubumbashi, the capital of the DRC's Copperbelt region, to Dar es Salaam through Zambia is substantially shorter than the distance to Mombasa through the Northern Corridor. If the Central Corridor railway reaches Isaka and connects to the Rwandan and Burundian networks, and if the Tanzania Zambia Railway Authority's TAZARA line, which connects Dar es Salaam directly to the Zambian Copperbelt, is rehabilitated to the standard required for heavy mineral cargo, Tanzania's claim on DRC and Zambian mining export trade becomes structurally compelling.

[VERIFICATION NOTE: Current TAZARA rehabilitation status and cargo volumes, and whether rehabilitation financing has been secured and construction commenced as of 2025, should be verified before publication. TAZARA has been in rehabilitation discussions for several years with Chinese and other financiers.]

LAPSSET's route to the DRC requires the full completion of the railway to Isiolo and the connection through Uganda, which is not in the current LAPSSET programme scope, or relies on a combination of road and rail that cannot match an integrated railway connection for bulk mineral cargo economics. The corridor competition for DRC mining trade is therefore one that Tanzania is better positioned to win under current infrastructure trajectories, and that position will become more durable with each year that Tanzania's SGR extension progresses and LAPSSET's railway component remains incomplete.

The Mombasa Capacity Question: LAPSSET's Original Commercial Justification

The original business case for Lamu Port rested substantially on a capacity argument. The 2017 LAPSSET status report included projections showing Mombasa Port reaching its expansion capacity around 2026, after which regional trade demand would exceed Mombasa's ability to handle it. This projected capacity constraint was the commercial foundation for Lamu Port: it would absorb the overflow that Mombasa could not handle, and the certainty of that demand would justify the investment in port, railway, and pipeline infrastructure.

The 2026 horizon referenced in the original projections is now the current year. The capacity constraint argument deserves reassessment in light of what has actually happened at Mombasa and in regional trade volumes over the intervening years.

[VERIFICATION NOTE: Current Mombasa Port throughput, capacity utilisation, and expansion status as of 2025 to 2026 should be verified against Kenya Ports Authority latest data before publication. This is a critical verification because the capacity argument is the commercial foundation of LAPSSET's Lamu Port investment case.]

What can be said on the basis of available knowledge is that Mombasa Port has undergone substantial investment and capacity expansion since 2017, including the development of the Kipevu Container Terminal which has added significant container handling capacity to the port's total throughput. Whether this expansion has been sufficient to handle actual trade growth, or whether the capacity constraint the LAPSSET projections anticipated is materialising, is a question that current data can answer and that materially affects the assessment of Lamu Port's commercial position.

What LAPSSET Can Still Win

The analysis above should not be read as a conclusion that LAPSSET has failed or that its strategic rationale has been permanently undermined. The corridor retains genuine and significant opportunity that the execution delays have deferred but not eliminated.

The Ethiopian connection is the most immediately actionable opportunity. Ethiopia's economy has been growing at rates that make it one of Africa's most significant trade markets, and its import and export volumes will continue to grow as industrialisation proceeds. The completed Isiolo to Moyale highway provides a functioning road connection. If the railway follows and LAPSSET can demonstrate competitive transit times and costs for Ethiopian cargo compared to the Djibouti route, the scale of Ethiopia's trade volumes means that even a meaningful minority share of Ethiopian transit trade would generate substantial cargo for Lamu Port and commercial viability for the corridor infrastructure.

The oil export logic retains relevance if the Lokichar to Lamu pipeline is eventually completed. Kenya's upstream oil development has been slower than originally projected, but the reserves exist and the development trajectory, while delayed, has not been abandoned. A functioning crude export pipeline would transform Lamu Port's economics and create the captive cargo base that the port's investment case originally depended on.

The northern Kenya development logic, opening the 70 percent of Kenya's land mass that lies north of the existing economic corridor to agricultural, pastoral, mineral, and tourism economic activity, remains valid regardless of the regional transit competition with Tanzania. The value of road and infrastructure access to northern Kenya is a domestic development dividend that exists independently of whether LAPSSET wins regional transit trade from Tanzania.

The special economic zone and industrial park infrastructure along the corridor, if developed with serious investment and policy support, could generate the domestic cargo production that reduces LAPSSET's dependence on transit trade and creates a self-sustaining economic rationale for the corridor infrastructure.

The Strategic Lesson in the Competition

The LAPSSET versus Central Corridor competition illustrates a principle that applies across East Africa's infrastructure landscape and that Uchumi360 has documented in multiple contexts. Infrastructure is not neutral. The corridors that get built, operated, and improved first become the corridors that capture trade flows, build logistics ecosystems, and develop the commercial viability that justifies further investment. The corridors that are planned but incompletely executed lose trade flows to competitors, see their commercial case weaken as projected cargo volumes flow elsewhere, and face an increasingly difficult financing environment as the uncertainty about their eventual completion compounds over time.

Tanzania's Central Corridor has benefited from this dynamic. It was not necessarily a better-conceived infrastructure programme than LAPSSET in its original design. But it has been executed more consistently, with railway investment that has progressed in stages, port investment that has delivered measurable throughput improvements, and a logistics ecosystem that has deepened as cargo volumes have grown. The compound effect of consistent incremental investment over a decade, while LAPSSET has navigated its execution challenges, has shifted the competitive balance in ways that are now structural rather than temporary.

For Kenya, the lesson is that LAPSSET's window for capturing its intended regional position is narrowing rather than remaining open indefinitely. The Ethiopian connection, the crude oil pipeline, and the railway completion are not components that can be deferred indefinitely without permanent consequences for the corridor's competitive position. Each year of delay is a year in which regional trade flows, logistics relationships, and supply chain infrastructure investment decisions are being made around a Central Corridor assumption rather than a LAPSSET assumption, and reversing those embedded decisions becomes progressively more expensive.

For the region as a whole, the corridor competition between Kenya and Tanzania is ultimately a positive dynamic if it produces better infrastructure, lower logistics costs, and more efficient connectivity for the landlocked countries whose economic development depends on access to ocean trade routes. The competition is most valuable when it accelerates investment on both corridors rather than producing a winner-takes-all outcome that leaves one corridor underutilised. East Africa's trade volumes are growing fast enough that both Mombasa and Dar es Salaam, both the Northern Corridor and the Central Corridor, can be fully utilised in a scenario where the investment in both is completed at the pace the region's growth trajectory justifies.

The question for Kenya's infrastructure planners is whether LAPSSET will be completed quickly enough to participate in that growth, or whether the corridor that was conceived as Kenya's second strategic gateway will become instead a monument to the distance between infrastructure ambition and infrastructure execution.

_______________________________________________________________________________________

Sources: LAPSSET Corridor Development Authority Status Report 2017, Kenya Ports Authority Annual Reports, Tanzania Ports Authority Annual Reports, Tanzania Railway Corporation SGR Project Documentation, TAZARA Annual Reports, Kenya Revenue Authority Trade Statistics, East African Community Trade Reports, African Development Bank Transport Infrastructure Assessment 2024, World Bank East Africa Trade Facilitation Report 2023, Tullow Oil Kenya Operations Disclosures, Kenya Pipeline Company Annual Reports.

_______________________________________________________________________________________

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

*Cover Photo Credit: Tanzania Invest

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.